Australia's inflation rate is to go monthly. Be careful what you wish for

- Written by: John Hawkins, Senior Lecturer, Canberra School of Politics, Economics and Society, University of Canberra

Australia’s consumer price index is about to go monthly, meaning Australia will join most of the developed world in getting an update on inflation at the end of every month, instead of once every three months as at present.

Until now Australia has been the only member of the Group of 20 leading industrial nations not to provide monthly updates, and one of only two members of the Organisation for Economic Co-operation and Development, the other being New Zealand.

It has been a particular concern for the Reserve Bank, which meets monthly to set interest rates based on its assessment of inflation, but gets the inflation figures only quarterly, and with a lag.

Laughing stock

Many of the prices are collected monthly but “not published until as much as three months later, and then only as part of a quarterly average,” the Bank complained in one of its missives to the Bureau of Statistics.

In June the governor told a Swiss audience about Australia’s “bad difference” and was met with incredulous giggles. “You may laugh”, he said.

Until now it’s been too expensive to produce monthly figures. Traditionally many of them have been collected by hand, though Bureau of Statistics “shadow shoppers” entering supermarkets and other stores and writing down the prices they see or recording them on handheld devices.

But scanner data, web scraping, and reports from service stations on petrol prices and real estate agents on rents have automated much of the process.

Tuesday’s information paper says items making up 43% of the consumer price index are already collected monthly or more frequently.

More frequent, more volatile

The new monthly index, to be published alongside the quarterly index, will include updated prices for items comprising 62-73% of the quarterly index.

It will be more volatile, and will not always provide a better guide.

A “dummy run” presented on Tuesday showed that in early 2022 a monthly index would have provided advance warning that inflation was rising.

But in late 2019/early 2020 the monthly index suggested inflation was rising sharply when the quarterly index turned out not to.

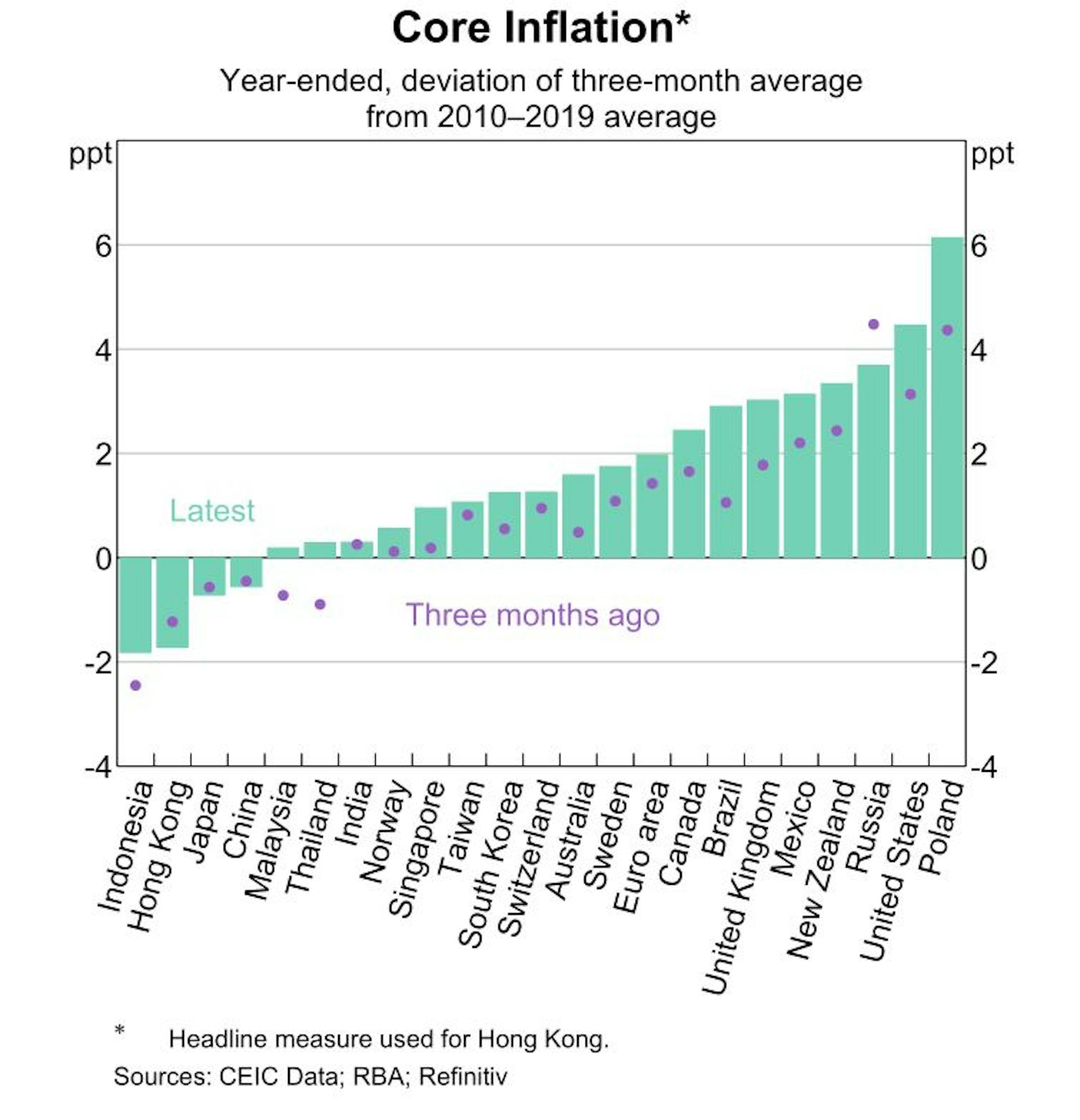

The monthly swings often reflect swings in the volatile prices such as petrol, fruit and vegetables rather than underlying trends. The prices of things such as international travel move in a saw-tooth pattern.

The Bureau of Statistics recommends against placing too much weight on month-to-month changes. The Reserve Bank avoids this when analysing inflation in other countries, averaging out monthly inflation into three-month blocks.

In the US last month, the net price increase was zero, but it didn’t portend annual inflation of zero.

The Melbourne Institute already produces a monthly Australian inflation gauge but it isn’t much quoted, perhaps for this reason.

Too much information?

One plus (or minus) with the monthly index is that it will be revised in the light of new or delayed information. The quarterly index is hardly ever revised, because it is used in contracts and the indexation of government benefits.

In a speech entitled Economic news: do we get too much of it? former Reserve Bank Governor Ian Macfarlane expressed doubt about the usefulness of monthly rather than quarterly information.

He said it enabled reporters to report how something “soared one month, then plunged the next one before soaring again” but could disguise rather than reveal what was really happening.

Read more: Inflation hasn't been higher for 32 years. What now?

And the monthly index might create the impression there’s more inflation than there is. Behavioural economics says people are loss averse. They pay more attention to bad news than good news. The monthly figures will present inflation news 12 times a year.

The media might amplify things. When the monthly change is high they might succumb to the temptation to “annualise” it, multiplying by 12, presenting an alarming, but misleading, picture, and not bother when monthly inflation is low.

The Reserve Bank’s task of restraining inflationary expectations might be about to become harder.

Authors: John Hawkins, Senior Lecturer, Canberra School of Politics, Economics and Society, University of Canberra

{kind=link}