Explainer: how our understanding of risk is changing

- Written by: Robert Hoffmann, Professor of Economics, RMIT University

Under the traditional notion of risk, people react predictably based on how risk-tolerant they are. Here, risk is calculated by combining the probability of something occurring (such as rolling a six with a pair of dice) with the value of the outcome (how much you have wagered).

But our understanding of risk is changing. We now know that a whole host of factors, from your personal history to your mood and age, all come to bear on how you perceive and take on risk.

For example, it is well known that investing in relatively high-risk stocks yields much higher returns than investing in relatively low-risk bonds. In the last 100 years US stocks have produced an 8% average annual real return compared to 1% return for more riskless securities.

But investors favour the safer securities despite the lower returns. This is called the equity premium puzzle. Put simply, more people should be investing in stocks.

Read more: Financial gamble? My brain made me do it

One influential theory suggests that people overestimate small probabilities and hate losses more than equivalent gains. This means that rare events such as winning a lottery are treated as much more likely than they really are.

It also means that people won’t participate in a coin flip where they win $10 for heads but lose $10 for tails. Most people will only play if they win $20 on heads and lose $10 for tails.

What influences risk

Research now shows that a whole range of factors influence risk-taking and perceptions. Sleep deprivation, for example, increases risk-taking as it depletes the ability to think logically.

Life experience, such as having lived through a recession or boom, also has an impact. For instance, those who lived through a recession are more pessimistic about future stock market returns and are less likely to own stocks.

This is because people make decisions based on their (limited) experiences rather than on objective analyses of risk and return, the present and future.

Other research suggests that people often rely on simple rules of thumb when choosing between options with uncertain outcomes. When it comes to investing, this means that people may simply choose the highest possible gain or smallest possible loss, ignoring probability altogether.

Your emotional state also affects risk perception, as does how you found out about the risk (did your friend tell you or did you find out from the news?). Researchers have even found the source of the risk is important to our perceptions. For instance, people perceive risk differently if the threat is coming from another person (in the form of humiliation or disapproval etc) rather than an impersonal force.

There are also cultural differences in risk attitudes. For example, in one study, Chinese people were found to be more risk-tolerant than Americans, contrary to what both groups believed. Some researchers have even constructed a world map based on risk attitudes.

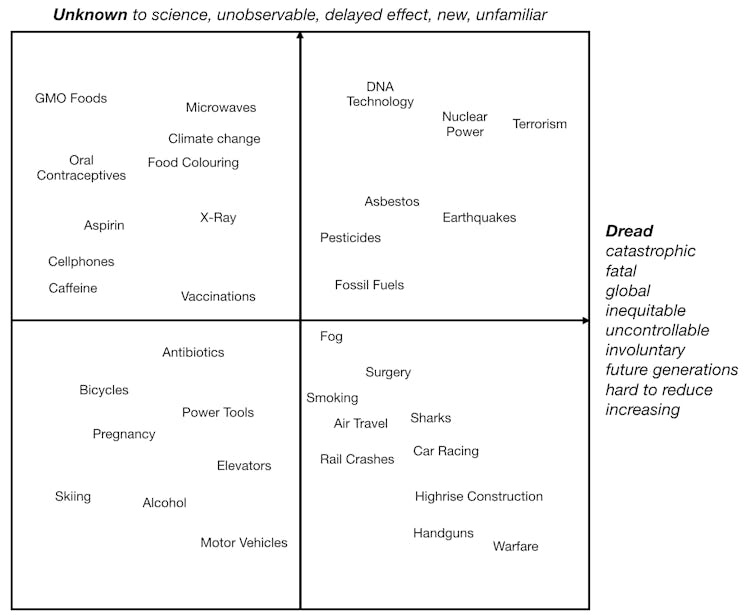

Finally, people tend to perceive risks along two emotional dimensions. “Dread risk” is associated with a lack of control and consequences that are likely to be catastrophic or fatal. “Unknown risk” relates to new, involuntary activities that are poorly understood.

As you can see in the following chart, terrorism is high on both dimensions, guns are high only on dread risk, and genetically modified foods are high only on unknown risk.

Unknown vs Dread Risks. Author provided.

Unknown vs Dread Risks. Author provided.

Recent behavioural economics thinking helps us to explain the equity premium puzzle: investors hate losses more than equivalent gains and tend to take too short-term a view of their investments. As a result, investors over-react to short-term losses and refuse to invest in high-risk stocks unless these have an extremely high return potential.

In a striking demonstration of this phenomenon, researchers recently carried out a 14-day experiment in which investors participated in a beta test of a trading platform. Half the investors had access to second-by-second changes in price and portfolio value. The other half could only see these changes every four hours.

The key finding was that investors with infrequent price information invested around 33% more in risky assets than investors with frequent information. As a result, those with infrequent information earned 53% higher profits.

Traditional economics suggests that more information is a good thing. These results reveal that more information actually hurts investment performance. This is because more information allows investors more opportunity to over-react to short-term losses.

What this all means

Our new understanding of risk has implications for our understanding of such varied contexts as housing markets, labor markets, customer reactions to services, choice between medical treatments, and even winners of US presidential elections.

It also turns out that someone who takes risks looks remarkably similar to a stereotypical Wall Street trader – young, smart, male, affluent and educated.

Funnily enough, even physical features like height and the ratio of your second and fourth fingers are predictive of risk-taking, because of the underlying genetic and hormonal factors that affect risk attitudes.

Insurance companies increasingly profile people using behavioural insights to work out premiums that reflect policy risks. One day finger ratio scans and personality tests may become a standard part of policy application forms.

Authors: Robert Hoffmann, Professor of Economics, RMIT University

Read more http://theconversation.com/explainer-how-our-understanding-of-risk-is-changing-79501