Climate change is a financial risk, according to a lawsuit against the CBA

- Written by: Anita Foerster, Senior Research Fellow, University of Tasmania

The Commonwealth Bank of Australia has been in the headlines lately for all the wrong reasons. Beyond money-laundering allegations and the announcement that CEO Ian Narev will retire early, the CBA is now also being sued in the Australian Federal Court for misleading shareholders over the risks climate change poses to their business interests.

This case is the first in the world to pursue a bank over failing to report climate change risks. However, it’s building on a trend of similar actions against energy companies in the United States and United Kingdom.

Read more: Why badly behaving bankers will never fear jail time

The CBA case was filed on August 8, 2017 by advocacy group Environmental Justice Australia on behalf of two longstanding Commonwealth Bank shareholders. The case argues that climate change creates material financial risks to the bank, its business and customers, and they failed in their duty to disclose those risks to investors.

This represents an important shift. Conventionally, climate change has been treated by reporting companies merely as a matter of corporate social responsibility; now it’s affecting the financial bottom line.

What do banks need to disclose?

When banks invest in projects or lend money to businesses, they have an obligation to investigate and report to shareholders potential problems that may prevent financial success. (Opening a resort in a war zone, for example, is not an attractive proposition.)

However, banks may now have to take into account the risks posed by climate change. Australia’s top four banks are heavily involved in fossil-fuel intensive projects, but as the world moves towards renewable energy those projects may begin to look dubious.

Read more: How companies are getting smart about climate change

As the G20’s Taskforce on Climate-Related Financial Disclosures recently reported, climate risks can be physical (for instance, when extreme weather events affect property or business operations) or transition risks (the effect of new laws and policies designed to mitigate climate change, or market changes as economies transition to renewable and low-emission technology).

For example, restrictions on coal mining may result in these assets being “stranded,” meaning they become liabilities rather than assets on company balance sheets. Similarly, the rise of renewable energy may reduce the life span, and consequently the value, of conventional power generation assets.

Companies who rely on the exploitation of fossil fuels face increasing transition risks. So too do the banks that lend money to, and invest in, these projects. It is these types of risks that are at issue in the case against CBA.

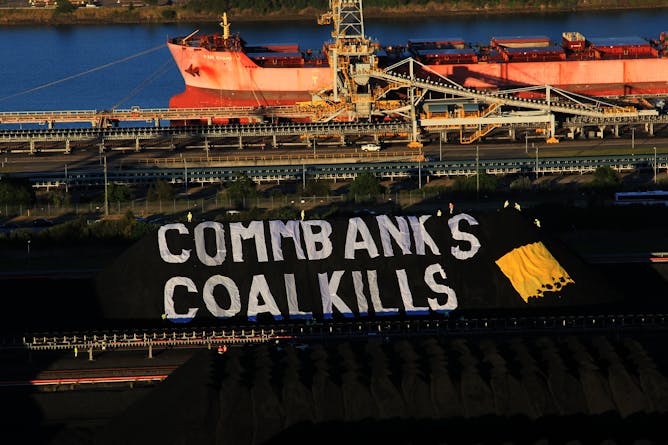

Greenpeace activists in May 2017 unveiled a giant banner on Newcastle coal stockpiles in NSW, calling on the Commonwealth Bank to stop investing money in coal.

AAP Image/Dean Sewell

Greenpeace activists in May 2017 unveiled a giant banner on Newcastle coal stockpiles in NSW, calling on the Commonwealth Bank to stop investing money in coal.

AAP Image/Dean Sewell

What did the CBA know about climate risk?

The claim filed by the CBA shareholders alleges the bank has contravened two central provisions of the Corporations Act 2001:

companies must include a financial report within the annual report which gives a “true and fair” view of its financial position and performance, and

companies must include a director’s report that allows shareholders to make an “informed assessment” of the company’s operations, financial position, business strategies and prospects.

The shareholders argue that the CBA knew – or ought to have known – that climate-related risks could seriously disrupt the bank’s performance. Therefore, investors should have been told the CBA’s strategies for managing those risks so they could make an informed decision about their investment.

Read more: We need a Royal Commission into the banks

The claim also zeros in on the lengthy speculation over whether the CBA would finance the controversial Adani Carmichael coal mine in Queensland. (The bank has since ruled out financing the mine.) The shareholders assert that the resulting “controversy and concern” was a major risk to the CBA’s business.

Global litigation trends

While the CBA case represents the first time worldwide that a financial institution has been sued for misleading disclosure of climate risk, the litigation builds on a broader global trend. There have been a number of recent legal actions in the United States, seeking to enforce corporate risk disclosure obligations in relation to climate change:

Energy giant Exxon Mobile is currently under investigation by the Attorneys General of New York and California over the company’s disclosure practices. At the same time, an ongoing shareholder class action alleges that Exxon Mobile failed to disclose internal reports about the risks climate change posed to their oil and gas reserves, and valued those assets artificially high.

Similar pathways are being pursued in the UK, where regulatory complaints have been made about the failure of major oil and gas companies SOCO International and Cairn Energy to disclose climate-related risks, as required by law.

In this context, the CBA case represents a widening of litigation options to include banks, as well as energy companies. It is also the first attempt in Australia to use the courts to clarify how public listed companies should disclose climate risks in their annual reports.

Potential for more litigation

This global trend suggests more companies are likely to face these kinds of lawsuits in the future. Eminent barrister Noel Hutley noted in October 2016 that many prominent Australian companies, including banks that lend to major fossil fuel businesses, are not adequately disclosing climate change risks.

Hutley predicted that it’s likely only a matter of time before we see a company director sued for failing to perceive or react to a forseeable climate-related risk. The CBA case is the first step towards such litigation.

Authors: Anita Foerster, Senior Research Fellow, University of Tasmania