Why would you dump a requirement for financial advisers to give advice that's in their client's best interests?

- Written by: Ama Samarasinghe, Lecturer, RMIT University

The findings about advisers in the landmark 2019 financial services royal commission couldn’t have been more stark.

Time after time financial advisers were found to have:

lacked skill and judgement

proposed actions that benefited the adviser

been unwilling to find out whether poor advice had been given

been unwilling to take timely steps to put bad advice right.

The result was a series of radical, but long-awaited changes in the industry, ranging from mandating a bachelor’s degree to enforcing ongoing professional development to introducing a legally-enforceable code of ethics.

Around 10,000 of the industry’s 25,000 advisers left, most retail banks offloaded their advice arms, and the median annual fee for ongoing advice climbed 40% from A$2,510 to $3,529.

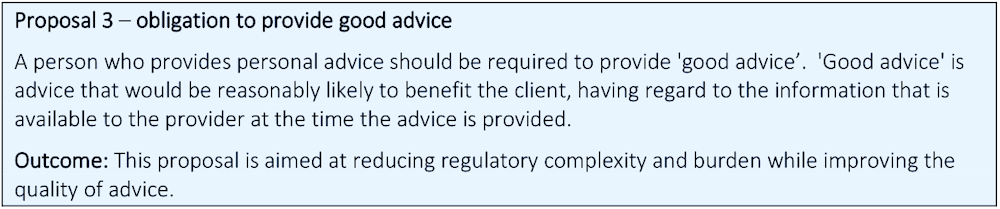

‘Best interests’ or ‘good advice’?

In response, ahead of this year’s election the then financial services minister Jane Hume commissioned a quality of advice review, which is due to hand its final report to the new financial services minister Stephen Jones on Friday.

Ahead of its final report the review has published 12 draft proposals intended to make advice more affordable and accessible.

One of them would replace the present requirement for advisers to give advice that is in their clients “best interests” with advice that is merely “good advice”.