The housing boom propelled inequality, but a coronavirus housing bust will skyrocket it

- Written by: Ilan Wiesel, Senior Lecturer in Urban Geography, University of Melbourne

A housing boom that lasted from the mid-1980s with only minor interruptions has added to rising income inequality in Australia. Yet an impending housing market bust, triggered by the coronavirus pandemic and the resulting spike in unemployment, will not restore greater equality. On the contrary, recent history shows housing busts can worsen inequality.

Those who benefit most from a boom are not those who pay the price when it busts. And those harmed by the boom often become even more vulnerable during the bust.

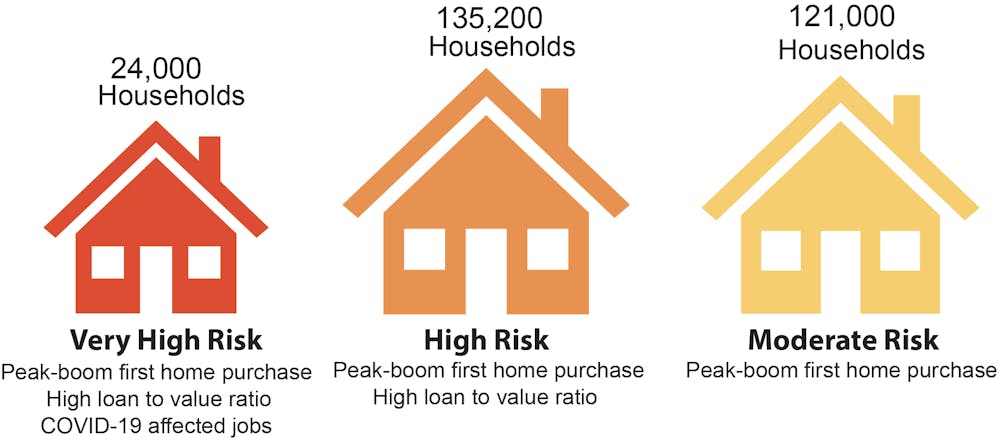

Our analysis highlights the risks for people who bought their first home at the peak of the boom. We estimate 24,000 households are at very high risk because they took out large loans that might soon exceed their home value and also work in sectors with high job losses. Another 135,200 are at high risk and 121,000 are at moderate risk.

Read more: How the housing boom has driven rising inequality

Coronavirus has set up a housing bust

Experts have long cited an upsurge in unemployment as the main threat to house price growth. This risk became reality with the coronavirus pandemic. Over the seven weeks from mid-March to early May, jobs fell by 7.3%.

Unless employment rapidly recovers, the housing market is facing a major downturn. In one worst-case scenario released by the Commonwealth Bank, house prices could fall by up to 32% over the next two years.

Recent first-time buyers are most vulnerable

Households that can hold on to their homes and weather the storm until the market recovers are not substantially harmed. Established owners, who bought their homes before or early in the boom years, have enjoyed the largest increase in their home values, and the largest reductions in their debt. This puts them in a position of relative resilience to a housing market bust.

Read more: Why falling house prices do less to improve affordability than you might think

In contrast, evidence from the 2008 housing crisis in the United States shows which households are most at risk. These were households that bought their first home with no deposit, or a very low one, in the period leading up to the 2008 crash. The crash left these households “underwater”, trapped with an asset worth less than their mortgage debt. Many defaulted on their mortgages, fuelling the housing market’s downward spiral.

The Australian housing market and financial institutions differ from those in the United States in 2008 in fundamental ways. Still, Australian households that bought their houses at the peak of the boom and have now lost their jobs in the coronavirus pandemic are facing the highest risk.

These include 24,000 recent (2014-5 to 2017-18) first home buyers who borrowed over 80% of the value of their home and were employed in industries where jobs have now collapsed. Another 135,200 recent first home buyers with high loan-to-valuation ratios are also at risk of going “underwater”, with homes worth less than their debt. Many of them are also in precarious employment, irrespective of the pandemic. (These figures do not include first home buyers in 2018-19, for which data are not yet available.)

Recent first home buyers at risk in a COVID-19 housing bust.

Source: Liss Ralston; data from ABS Survey of Income and Housing 2014-5 to 2017-8

Recent first home buyers at risk in a COVID-19 housing bust.

Source: Liss Ralston; data from ABS Survey of Income and Housing 2014-5 to 2017-8

Read more: Build social and affordable housing to get us off the boom-and-bust roller coaster

Renters’ relief could be short-lived

Many private renters hope a housing downturn will translate into lower rents and perhaps give them a chance to buy their first home in a more affordable market. However, this is not always the case in a downturn. In the US from 2007 to 2009, despite declining house prices, rental affordability stress has only increased.

In Australia, the sudden decline in international students and short-term rentals has increased long-term rental vacancies in some areas. Reports suggest rents are going down, especially at the upper end of some rental markets.

Read more: As coronavirus hits holiday lettings, a shift to longer rentals could help many of us

However, in the longer run, the slowdown in housing construction will create supply shortages, leaving rental vacancies low and rents high. Many landlords, mostly “mum and dad” investors, have taken large loans to finance their property investment. They will need to keep rents high to hold on to their investment properties.

Lower house prices will enable some households to become home owners for the first time, after being locked out of the market during the boom years. These households could benefit from a coronavirus housing bust if the market then recovers. Even so, their gains will do little to change the overall trend of rising inequality made worse by the housing downturn.

We need to flatten out booms and busts

Improved housing affordability is necessary to reduce social and economic inequality. A housing downturn will reduce house prices. But this downturn, when coupled with rising unemployment, will not deliver greater equality, especially if it’s followed by yet another boom.

Australia has flattened the curve of COVID-19 infections. To be successful in reducing inequality, we need to flatten the curve of both booms and busts in the housing market cycle. And only a thorough overhaul of national housing policy will achieve that.

Read more: Coronavirus lays bare 5 big housing system flaws to be fixed

Authors: Ilan Wiesel, Senior Lecturer in Urban Geography, University of Melbourne